In the past couple of trading sessions, the S&P index has almost stealthily surpassed the 4,000 point threshold to record yet another all-time high, as if it was the most natural thing in the world. But… we are into April, and wasn’t there supposed to be a sizeable market correction by now? I vividly recall many of the pundits and a good number of friends’ and colleagues’ alike running for the exits earlier in the year and sitting on a mountain of cash ever since, growing increasingly less confident by the day.

No matter what valuations are telling us, no matter what stock movements the so-called rotation trade is causing, no matter how many indicators have been screaming Sell from the rooftops, the broader stock market has confirmed its bullish mode. Even the tech sector that has fallen victim to a short-term correction in February has been forming a bottom of sorts and is on the verge of turning up again. The S&P above 4,000 couldn’t be a better testament to all this.

It’s not just the equity market. Wherever one looks, risk assets keep enjoying their bonanza. US corporate high yield bonds have just been marked at their tightest credit spreads since 2007. Commodities have evidently had their run. And even crypto knows no boundaries. As stock indices in combination with the Treasury market are telling us, risk is on, and risk-free is out for now. Whether the pundits want to hear it or not, it may well be different this time.

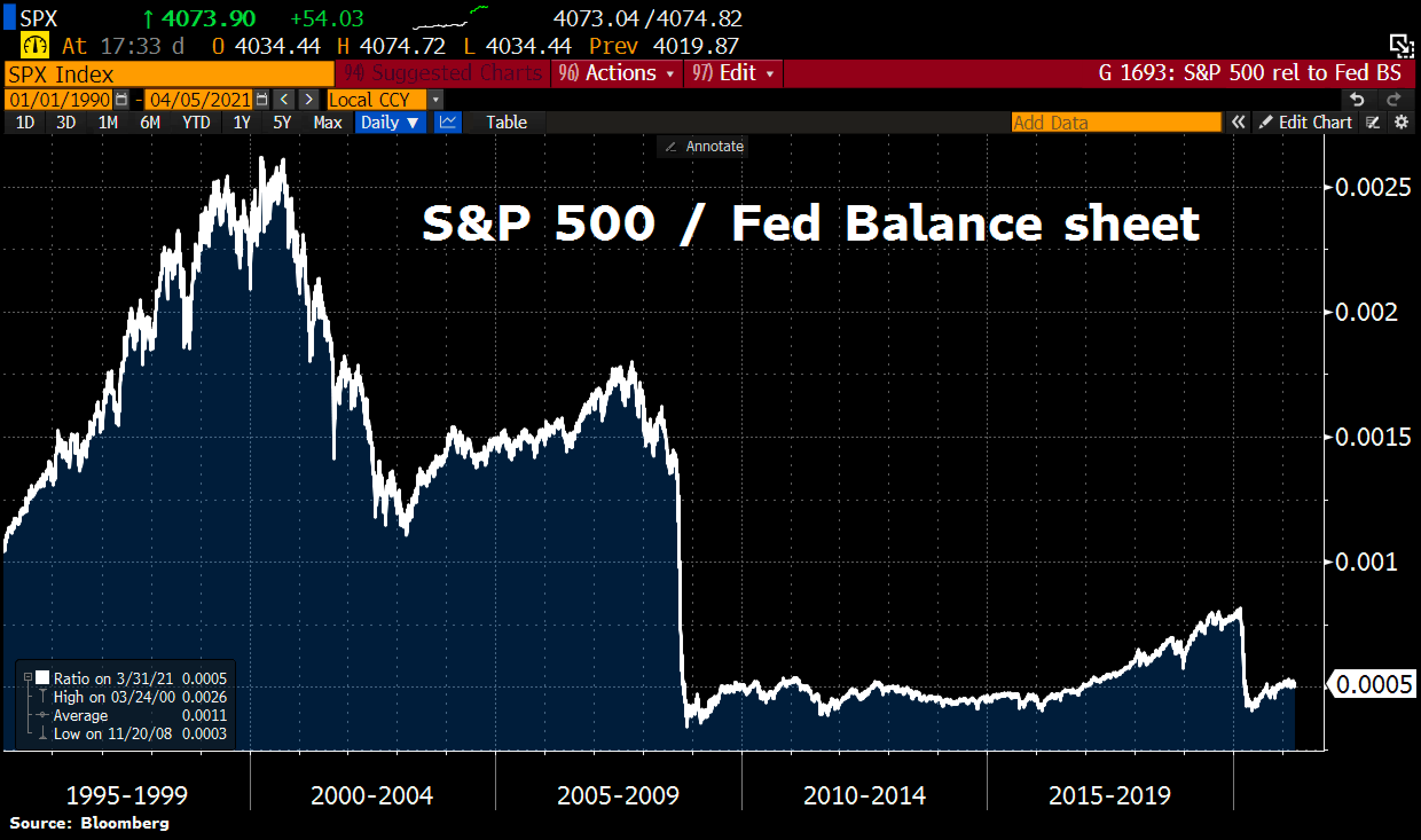

Now why on earth are asset prices defying gravity? Coming out of the Easter weekend I stumbled across this

chart on Twitter that may be providing the newest and simplest of explanations. It depicts the S&P500 in relation to the Fed’s balance sheet, and it shows that adjusted for the expansion of the money system since the break of the financial crisis equities have actually traded sideways for the past 12 years. So, where does that leave the overvaluation argument?

Moreover, applying the same measure the S&P traded at more than 3 times the current value before the financial crisis and at 5 times the current value before the dot-com bust. In other words, taking into account the gargantuan excess liquidity created by the Fed we are a long way from bubble territory. Quite the contrary seems to be the case. And considering that the Fed is not done printing by a mile, the ratio may even turn down again if the S&P were to pause or stop its ascent.

To be sure, the fact that the excess liquidity only marginally made its way into the real economy over the past decade and mostly sloshed around the financial system has certainly helped asset prices. If the Biden administration were to engineer the mother of all growth booms, this liquidity might well be withdrawn from financial assets to an extent and, as the rock-bottom velocity of money gets lifted, proportionately be mopped up by the underlying economic activity and related transaction mechanism.

However, in the scheme of things, this should not matter all too much. That the market will correct substantially at one point, maybe soon, is probably a given, but the secular trend of money creation supporting equity- and other risk markets should hold. Well, anything can happen of course, and it usually does, but I wonder whether some of my friends’ anticipated crash scenario, just because history has told us so, is not totally out of place here.